This week we cover scuttlebutt insights of six industries- Paints, FMCG, cigarettes, Cement, BFSI, and Textiles industry followed by what’s trending in markets and curated good reads.

Outline

1. Scuttlebutt insights on six key industries

As quoted by Philip Fisher, getting a reality check from the people associated with the company is crucial for deeper insights☝️ So, so here we explain what’s happening on the ground in Paints, FMCG, cigarettes, Cement, BFSI, and Textiles industries- curated from Philip capital’s “Road Less Travelled” report.

Industry 1: FMCG📦

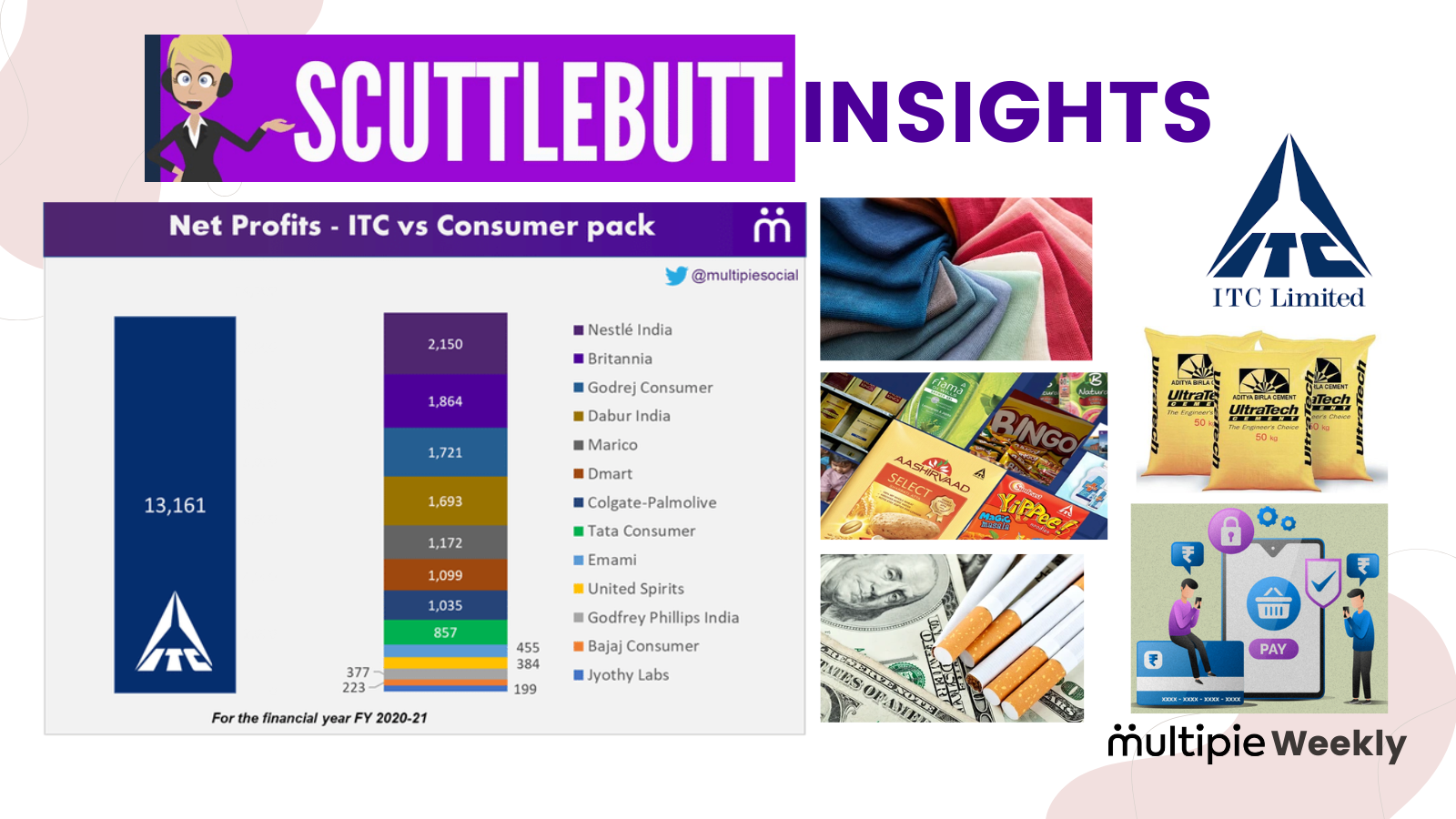

↪️ ITC

ITC is making new highs and is now everybody’s favourite stock 🙂 If you are wondering what changed about the stock, we explain here:

In ITC’s FMCG business, its Hygiene brand- Savlon is facing sales pressure; but the packaged food category is doing well. Here’s some extracts💁♀️..

i) Atta (Aashirvaad): Healthy growth rate experienced here, 3-4% price hike taken in last 12 months. Value-added sales contribute 10% of total sales.

ii) Yippee: Gaining market share from Maggi🏆 as the company didn’t take the price hike here compared to the Rs2 hike taken by Maggi.

iii) Biscuits & Bingo: Performing decently.

↪️ Emami & Zydus wellness:

Rural demand remains weak; poor traction in summer products & Balm portfolio. There is still a sign of relief in this segment till the time Jiomart doesn’t enter this area.

Industry 2: Cigarette 🚬

↪️ Cigarette volumes have recovered to pre-covid levels, with recovery driven by the premium segment. While ITC is already a market leader with a market share of ~78%, to further gain market share, ITC has launched 4 new brands of cigarettes- Players, Gold Flake Mixpod, Classic Connect, and Indie Mint.

- Trade terms & conditions are improving under the leadership of Devraj Lahiri (CEO of the cigarettes business). Dealers are no longer given impractical aggressive sales targets now & the focus is on maintaining competitiveness & high visibility.

Other competitors- GPI & VST industries which lost the market share in the past, are trying to make a comeback by launching aggressive schemes.

Industry 3: Cement industry🏗️

- Demand scenario: All the dealers are positive about the demand recovery in H2 2022 driven by infrastructure projects.

- Pricing: Prices usually remain constant in the north and western region whereas it is volatile in the south. Broadly, companies in all the areas might take price hikes due to cost pressures but comparatively, companies in the north are expected to have better profitability

- Adani’s entry into the industry will have the least impact on the southern market as it has negligible exposure there. Distributors from the other regions are not very sure about the impact.

Also lately, promoter buying is happening across more than 10 companies in the cement industry🙌

Industry 4: BFSI💰

↪️ Payments:

- Although UPI getting linked with credit cards is huge & will make the ecosystem much more efficient, the roll-out here will take time as groundwork needs to be done.

- MDR on UPI: To reach seamless transactions and avoid fraud at the same time, MDR in UPI has to be implemented. This will helps the likes of Paytm make revenue from merchants (highest inroads in merchants).

- Buy Now, Pay Later (BNPL) can work out really well, if the cost of funds is reasonable. To know more about BNPL and the company leading in this space, click here.

↪️Microfinance:

- Experts expect bad Q1FY23 due to new MFI regulations. During Q1 last year, the loans were disbursed to 72 lakh customers compared to 9.6 lakh customers in May 2022.

- Asset quality is expected to be decent. Collection efficiency on the paying book is 99%. PAR 30 on a new book is 0.3% for the industry.

- Loan rejection rates fell to pre-pandemic levels at 15% from a spike to 21% a few months ago😲

Industry 5: Textiles👚

- Textile players suffering due to high cotton prices & the industry wants the government to support this situation.

- The majority of the industry experts are forecasting the situation to sustain till October i.e. till the time cotton’s supply arrives in the market.

- This huge problem is also because of the low inventories with spinning mills.

- Mills are facing problems to pass on the high input costs, leading to a hit on profitability.

Industry 6: Paint industry🎨

Compelling demand:

Paints volumes are up 10% compared to 2019 in spite of hefty price hikes in the last 8-9months i.e. of 25%. This is due to a solid pickup in the construction of homes after the first covid wave. Especially premium products getting high traction.

Asian paints seizing the market share:

- Despite difficult situations and disruptions in the industry, Asian paints were able to increase its market share by introducing economy range products.

- Waterproofing and Putty industries were seeing extremely strong growth. So, Asian paints gave many lucrative schemes in these segments. The company has also appointed dedicated distributors, plumbers, carpenters & hardware stores to focus on new initiatives.

Other competitors- Akzo Nobel, Berger paints & Kansai Nerolac are struggling to retain their market shares due to frequent churn of distributors, lack of transparency in incentives/schemes & less focus on direct channels.

2. What else is trendin’?🤙🏻

✔️ Lenskart is ready to buy a majority stake in apan’s Owndays Inc. After this deal, the company will become Asia’s largest online eyewear retailer. Lenskart has valued Owndays at $400Mn.

After this deal, Lenskart will continue to focus on the mass-mid class segment whereas Owndays will target the high-premium segment. Peyush Bansal estimates $650Mn sales for both companies combined.

✔️ Government increase the import duty on gold by 5% i.e. it has increased to 12.5% from 7.5%. This is the reason all the jewelry tocks such as Titan, TBZ, Vaibhav Global, and Thangamayil jewellery tanked after the news

✔️Reliance industries fell last week. This reaction was because of the combination of 2 things: Change in leadership & announcement of taxes on the windfall gains earned by crude oil producers. You can read it in detail here.

✔️Export figures are positive for Pharma (+10%), textiles (+24%), and chemicals (+24%) on an MoM basis in May’22.

A lot of discussions are happening by the community on Multipie, be it sector-specific (Automobile–commercial vehicles, capital goods, Banking, etc) or be it personal finance or red flags in the companies.

You are definitely missing out on a lot if you are not on Multipie yet. So, join the community & become a better investor 😄

3. Good reads 📚

3.1 What to look for in management while analyzing a business

3.2 Daily stock updates. Follow Abhishek for the same.

3.3 Detailed thread on what’s happening to Iron Ore

3.4 Wonderful thread on “Learnings to improve your business

3.5 Why while valuing a DCF, the majority of the time the stock seems to be overvalued, and what can be done.

See you next week. Until then, happy investing!