Welcome to the 17th edition (13th on blog) of our weekly newsletter. Topics for this week include our market snapshot, thoughts on the National Asset Monetisation Pipeline, highlights from Edelweiss’ Small and Midcap model portfolio, some dope career advise, good reads and more. If you are finding these helpful, please spread a word about us by sharing with your friends and work network. Let’s get started.

Outline

1. Market snapshot – ‘Power’ packed week

The week that was: Power & Utilities (up 8.3%), Energy (up 3.6%) and Industrials (up 3.4%), were the best performing sectors, indicating an increasing bullishness in asset-heavy segments. The strength in Power & Utilities was driven by Adani Group stocks which were up between 12 and 28%. Last two quarter earning calls have painted a bullish outlook for Power/ Utilities and manufacturing segment, with expectations of significant improvement in capacity utilisations, driven by strong industrial and export demand.

Last 6 months: Top performing sectors for the last 6 months are IT, Commodities/ Materials and Power Utilities.

Large caps continued their outperformance over small and midcap segments. Have you reduced your smallcap allocations or holding on? Let us know.

2. Edelweiss Research: Small and Midcap model portfolio highlights

Edelweiss research released their Small and Midcap (SMID) strategy note last week. Their SMID model portfolio is categorized in 3 groups:

- Winners: Quality, market leadership, structural opportunities

- Warriors: Earnings recovery, cyclically favorable, category leaders

- Value: Potential re-rating candidates

Here are some key highlights of changes in model portfolio:

- Overall weights of Winners decreased from 31.5% to 22.5%, of Warriors remained same at 47.5%, but the weight of Value category has increased from 21% to 30%.

- Focus shift from the Buy at any price (BAAP) category to Growth at reasonable price (GARP) companies

- Winners: The two new entries are IEX and SIS India whereas the exits include Voltas, SRF, Exide Industries, TeamLease, Crisil, and TCl Express

- Warriors: New entries include JK Cement, Concor, Jindal Stainless, VIP, Trent, and CESC whereas the exits include Bajaj Electricals, IPCA and Mahindra Logistics.

- Value: New entries include KEl Industries, Mahanagar Gas, Federal Bank, GSPL, Suntech, Firstsource and Birlasoft, whereas the exits include Brigade Enterprises, Prince Pipes, and eClerx Services

Which of these companies do you like most? Let me know and I will share our thoughts and insights on them!

3. The National Asset Monetisation is crucial for economic revival

One key development last week was the announcement of National Asset Monetisation Pipeline (NMP) where the Government is looking to monetize public infrastructure assets and generate ~INR 6 lakh crores over the next 4 years. While this will be no easy task, I believe this is a step in the right direction. Let’s discuss some key highlights:

- Monetization is not the same as divestment.

Ownership of the assets remain with Government and the rights for identified assets will be handed over to private players to operate and maintain for a defined period. The private players will pay an upfront consideration in exchange for the right to use these assets. Revenues and benefits from these assets during the concession period remains with the private players.

In effect, the government is telling private companies that here are these ready road, railway platform, warehouse, gas pipeline, ports that you can operate for 20-25 years. Please calculate what you can earn from it during this period, discount that cash flow to its present value, deduct from that your profit margin, and pay us the balance amount as upfront rental.

- Which assets are being monetized?

Core revenue-generating assets of the government (details in chart above). Take road sector – total length of national highway assets is estimated to be about 1,21,155 km. NMP proposed to monetize 26,700 km constituting nearly 22% of total NHs. Monetization of non-core assets (land, building) and disinvestment is not included in NMP. Expected inflows over next four years – 15% in FY22, followed by 27%/ 30%/ 28% in FY23/ 24/ 25 – INR 880 Bn/ INR 1.6 Tn/ INR 1.8 TN/ INR 1.7 Tn for FY22-25.

- Why monetize?

The NMP will finance 5.5% of the overall spend and ~17% of the greenfield Capex planned under the ambitious INR 110 trillion National Infrastructure Pipeline(NIP). While traditional infrastructure funding routes (union govt spending, debt, private capital etc) and hopefully upcoming DFI will do the heavy lifting, asset recycling through NMP will help in bridging the gap, while India’s Debt-to-GDP normalizes. The impact of pandemic has taken India’s Debt to GDP ratio to multi-year highs of over 60% and incessant borrowing is not an option given our borderline sovereign rating of BBB-. Government owns many inefficient public assets today and hopefully NMP will revive them via private sector participation. The future needs Gigafactories and new investments in Semiconductor, AI, Robotics and monetization now becomes the key.

- Expected GDP multiplier:

Public infrastructure investment has proven to be the most effective in increasing economic output compared to other forms of public spending. If the Indian economy has to bounce back towards double-digit GDP growth, Banking credit expansion and Infrastructure growth will have to play a key role. We need public-private capex and greenfield expansion now. Note that investment-led growth was the key to China’s dominance in last 2 decades.

- NMP can revive Capex cycle and drive Banking credit growth:

Indian economy needs a revival of “animal spirits” after a lost decade of fresh capex. There are many reports talking of India Inc nearing a fresh Capex cycle akin to 2002-2008, but for that breaking out of the financing conundrum is the key.

The NMP might face operational challenges and the execution remains to be seen, but I concur with EY’s Infrastructure practice partner Abhaya Pandey that the NMP will be a game changer for infrastructure investment in India.

4. Some career advise that I liked – 7 high-value ideas and habits

Here is something powerful I read on career growth from Shreyas (recommend you to follow) in a thread titled 7 high value ideas & habits that took him more than a decade to learn:

- Most Execution problems are actually Strategy problems, Interpersonal problems, or Culture problems. Fix the root problem.

- You can think of your work at 3 levels – The Impact level, the Execution level, the Optics level. Each level is important. But the level at which you think by default matters a lot. Owners fixate on the Impact level, Doers fixate on the Execution level, Politicians fixate on the Optics level.

- Both strategy and execution matter. When you genuinely care about something, you focus much more on impact than on optics. People who genuinely care about Execution care a lot about their Strategy and vice versa.

- Problem solving is a misnomer. Solving one problem creates another set of problems. Do not try to eliminate all problems. Instead it’s wiser to pick what problems we are willing to live with.

- Be careful with “Under-Promise and Over-Deliver”. Under-Promise & Over-Deliver is a good policy for setting external expectations e.g. with customers, investors. It is a terrible practice for setting personal goals because it builds the habit of aiming lower than our potential.

- When picking companies to work at or to invest in over the long-term, pay a lot of attention to Culture, People, Momentum, and Market. We overestimate short-term challenges and underestimate the effect of Market & Momentum.

- To create outsized outcomes for your company & for yourself – stop doing work that simply provides a positive Return on Investment. Create a habit of focusing on work that minimizes Opportunity Cost. ROI thinking favors quick wins. Opportunity Cost thinking favors big wins.

5. Visual weekly – Some interesting charts

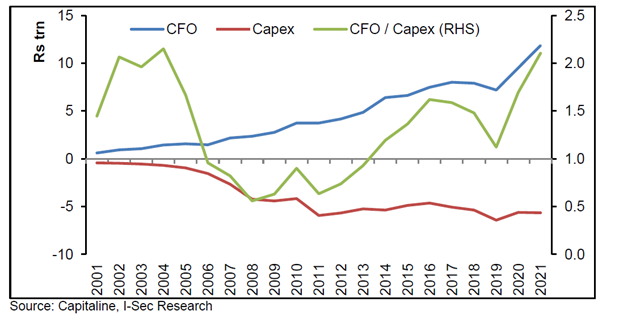

5.1 Operating Cash Flows to Capex at two decades high

The ratio of cash flow from operations to capital expenditure for Indian companies has reached 2.2 times, the highest level in two decades. The last time this happened was at the beginning of the previous capital expenditure cycle in 2002.

5.2 Indians spend equal time on short format video apps as on OTT platforms

In 2022, an average Indian is expected to spend as much time on short format video apps (Moj, Josh, MX Takatak, etc) as on OTT platforms such as Netflix, Prime, etc. Not sure how I feel about this one. Source: The-Ken

5.3 India versus China working-age trajectory

China formally revised its laws and now allows couples to have up to three children. This chart below tells you why – a decline in working age population.

6. Good reads and other news

1. The race for a Super-app – who will build India’s Wechat?

The Super-app race has been heating up with the race of Reliance, Tata and Adani groups to build India’s Wechat. However, a new draft rule bars related parties from selling on an online marketplace platform. The rules also restrict apps from having sellers that share brand names. For example: Tatas will not be able to sell its own products – like Tata Salt or Sampann – on its e-commerce platform like Bigbasket. Meanwhile, Reliance JioMart is aggressively marching with its Super-app plan and plans to unveil super app adding Just Dial offerings

2. Three eras of the internet and why decentralization matters. If you are a Crypto enthusiast, you must follow Chris Dixon . My favorite bit:

“Decentralized networks can win the third era of the internet for the same reason they won the first era: by winning the hearts and minds of entrepreneurs and developers.”

3. RenewPower is the first Indian Renewables company to list on the NASDAQ

4. Summary of SaaS bhoomi report on Indian SaaS landscape – a sunrise sector

5. TSMC, the world’s largest chipmaker is raising prices by as much as 20%. This is expected to make electronics costlier.

6. New drone rules make flying them easier and cheaper (IndianExpress)

7. Video of the week: Prof Damodaran – Statistics for Investors

Understanding how to use statistics has become critical in a world filled with opinions and bad data. Good news! Prof. Aswath Damodaran announced a free 13 session course of Statistics, with the focus primarily on applications in investing.

8. Tweet of the week

This simple tweet from Gaurav blew up this week and there is good enough reason. Peer to Peer lending (P2P lending) model which had a tainted past has made a comeback and how. Here is what happened:

- Recent unicorn BharatPe announced a new feature that allows users of the app to lend money to each other at an interest rate of up to 12% p.a.

- CRED then did one better with loans at 9% under CRED Mint!

- And someone saw an arbitrage opportunity 🙂

That’s all for this week. Please share with your peers if you found this helpful and subscribe to start receiving the weekly digest in your mail! Happy weekend!

Thoroughly enjoyed this